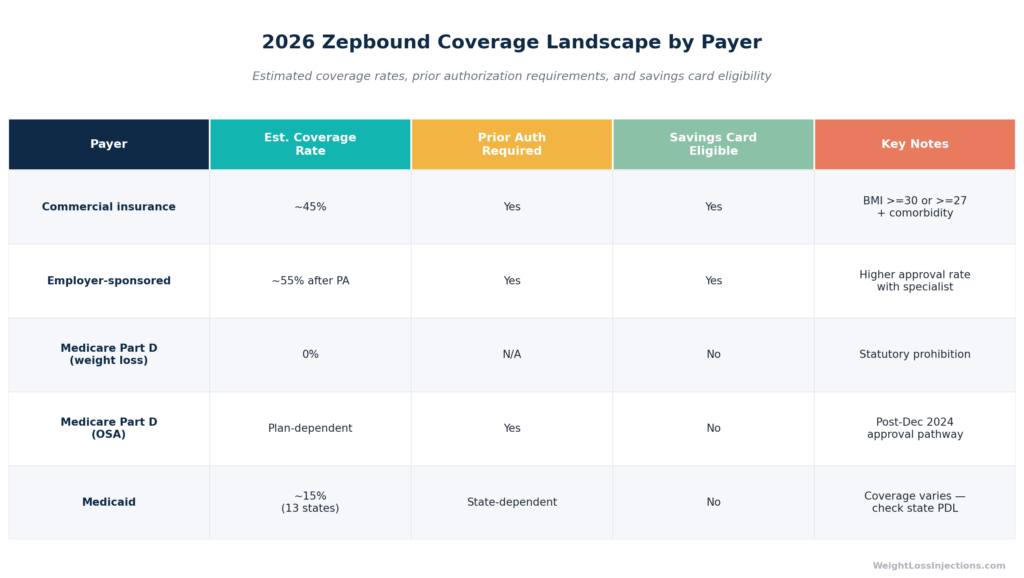

2026 Zepbound Coverage Landscape by Payer

Zepbound’s list price is $1,086/mo for all dose strengths. With commercial insurance that covers the weight-management indication plus Eli Lilly’s savings card, that drops to as little as $25/mo, though the 2026 annual savings cap has been reduced to ~$1,300 (down from $1,950 in 2025). Medicare Part D does not cover Zepbound for weight loss under any Part D plan, but a new OSA coverage pathway opened in December 2024, and the CMS Medicare GLP-1 Bridge program offers eligible Part D enrollees a $50/mo copay from July 1 through December 31, 2026. If your insurance doesn’t cover Zepbound, LillyDirect self-pay runs $299–$449/mo depending on dose.

Coverage Landscape at a Glance (2026)

About 43–45% of commercial insurance plans cover Zepbound for weight management as of early 2026. That number climbs to roughly 55% for employer-sponsored plans once prior authorization is secured. Outside commercial coverage, the picture is more constrained: Medicare Part D is statutorily barred from covering Zepbound for obesity, Medicaid covers it in only about 13 states, and government-insured patients cannot use Lilly’s savings card under any circumstances.

The table in Image 1 above maps each payer type at a glance. The sections below walk through each in depth, what drives approval, where the friction points are, and what to do when a claim is denied.

One number frames everything: the wholesale acquisition cost (WAC) for Zepbound is $1,086/mo for a 28-day supply regardless of dose strength. That list price is your baseline, insurance, savings programs, and direct-pay channels are the mechanisms that move it lower.

Commercial Insurance: What Determines Coverage

BMI and Comorbidity Requirements

Commercial plans that cover Zepbound align their prior authorization criteria closely with the FDA-approved indication language: adults with a BMI ≥30 kg/m², or adults with a BMI ≥27 kg/m² with at least one weight-related comorbid condition, such as hypertension, type 2 diabetes, or dyslipidemia. If your clinical profile matches this language exactly, you have the strongest foundation for a PA.

Mismatches between the ICD-10 codes on the PA form and the indication language are a leading cause of avoidable denials. Your prescriber’s office should confirm that the primary diagnosis code, E66.01 (morbid obesity due to excess calories), E11.9 (type 2 diabetes without complications), I10 (essential hypertension), or G47.33 (obstructive sleep apnea), is explicitly cited in the PA documentation and matches what is listed in your medical record.

Step Therapy Requirements

Step therapy is the insurer’s right to require documented failure on prior agents before approving Zepbound. The requirements vary significantly by payer:

- Kaiser Permanente NW: May require trial of ≥2 prior weight-management medications and up to 6 months of semaglutide before approving tirzepatide.

- Cigna and Aetna: Typically require ≥6 months of documented diet and exercise failure under medical supervision.

- UnitedHealthcare: Often requires an endocrinologist or obesity medicine specialist letter alongside BMI documentation.

If you have already tried semaglutide (Wegovy or Ozempic) or another GLP-1 agent and experienced inadequate response or intolerable side effects, document that clearly. It satisfies step therapy requirements and strengthens medical necessity arguments.

Major Insurer Summary (April 2026)

Based on Pandameds’ insurance coverage analysis from March 2026:

| Insurer | Est. Approval Rate | Common PA Requirements |

|---|---|---|

| UnitedHealthcare | ~52% | Endocrinologist letter + dated BMI measurement |

| Aetna | ~48% | ≥6 months diet/exercise documentation |

| Cigna | ~44% | OSA indication is favorable; step therapy typical |

| Blue Cross Blue Shield | ~40% | HTN or T2D comorbidity often required |

| CVS Caremark (PBM) | Formulary removed | File formulary exception — see below |

The CVS Caremark situation deserves specific attention. CVS Caremark — which manages pharmacy benefits for roughly 25–30 million commercially insured patients — removed Zepbound from its standard formulary effective July 1, 2025. Patients whose plans use CVS Caremark as their pharmacy benefit manager will not have Zepbound covered through standard channels. However, a formulary exception process is available: your prescriber submits a medical necessity letter explaining why Zepbound is clinically necessary for you specifically, and the plan reviews it outside the standard formulary. These exceptions are granted in a meaningful share of cases, particularly when a prior GLP-1 was tried and failed.

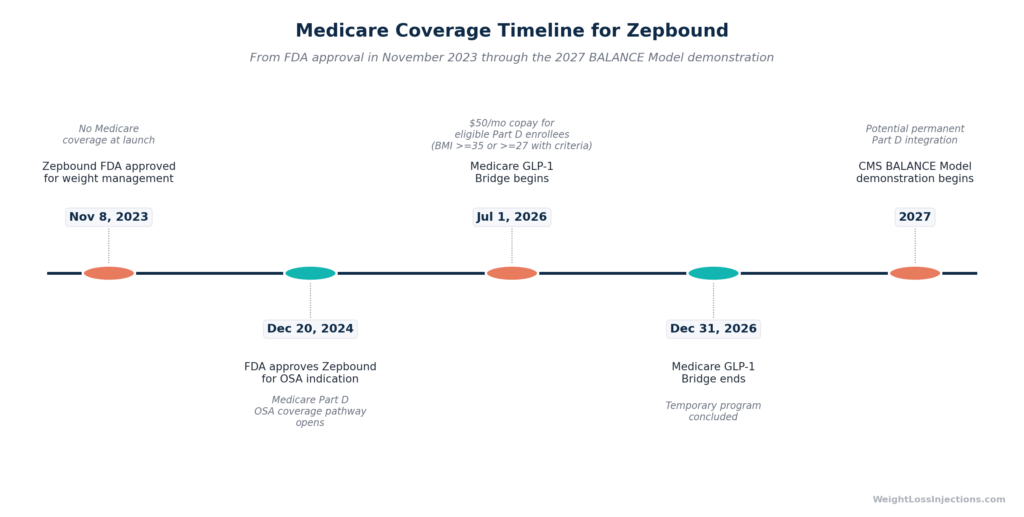

Medicare Coverage: What Changed in 2024 and 2026

Weight Loss Indication: Still Not Covered

Medicare Part D is statutorily prohibited from covering drugs used solely for weight loss, this dates to the original Medicare Prescription Drug, Improvement, and Modernization Act and has not changed as of April 2026. Regardless of your BMI, your duration of obesity, or how many prior treatments you have tried, no standard Part D plan can cover Zepbound for the weight management indication. This is not a formulary decision a plan can override — it is a federal statutory restriction.

There is no legislative fix on the immediate horizon. The Treat and Reduce Obesity Act has been introduced in multiple congressional sessions but has not been enacted. The most recent American College of Gastroenterology statement from April 2025 confirmed that anti-obesity medications will not receive full Medicare Part D coverage in 2026 under current law.

OSA Indication: A New Coverage Pathway

The landscape shifted on December 20, 2024, when the FDA approved Zepbound as the first and only prescription medicine for moderate-to-severe obstructive sleep apnea in adults with obesity. OSA is not a weight-loss indication, it is a discrete disease state, and Medicare Part D plans may now cover Zepbound when it is prescribed specifically for moderate-to-severe OSA.

The critical requirements for Medicare OSA coverage:

- An AHI (apnea-hypopnea index) of ≥15 events per hour documented by sleep study or equivalent evaluation.

- The prescription must explicitly cite the OSA indication — not obesity or weight management.

- Your specific Part D plan’s formulary must include Zepbound for the OSA indication (coverage is plan-dependent, not universal).

Contact your Part D plan directly and ask whether Zepbound is on the formulary for ICD-10 code G47.33 (obstructive sleep apnea). If it is not yet listed, your prescriber can submit a coverage determination request.

One critical restriction: the Eli Lilly savings card is not available to Medicare beneficiaries. Government-insured patients — including those on Medicare Part D, cannot use manufacturer discount programs. This exclusion is not a clerical matter; it is required under federal law. See the federal exclusion notice below.

Federal exclusion notice: The Eli Lilly Zepbound savings card, and any manufacturer coupon or copay-assistance program — cannot be used by patients whose prescriptions are covered by Medicare, Medicaid, TRICARE, the Veterans Administration, or any other federal or state government health care program. Use of such coupons by government beneficiaries implicates the federal Anti-Kickback Statute, 42 U.S.C. §1320a-7b, which prohibits offering or receiving anything of value to induce or reward federally reimbursed prescriptions. Patients in any government program must not present or use manufacturer savings cards at the pharmacy.

Medicare GLP-1 Bridge Program (July 1 – December 31, 2026)

Medicare Coverage Timeline for Zepbound

For Medicare beneficiaries who want Zepbound for obesity — not OSA — the CMS Medicare GLP-1 Bridge program is the only available pathway in 2026. According to KFF’s March 2026 analysis, CMS announced a short-term program under which Medicare will cover Zepbound and Wegovy for eligible Part D enrollees at a $50/month copayment for the obesity indication.

Key details of the Bridge program:

- Eligibility: BMI ≥35, or BMI ≥27 with qualifying clinical criteria.

- Copayment: $50/month per prescription.

- Duration: July 1, 2026 through December 31, 2026 — six months only.

- Outside Part D: The Bridge operates outside the standard Part D benefit structure. Spending under the Bridge does not count toward your 2026 Part D out-of-pocket cap of $2,100.

- What comes next: The Bridge transitions to the BALANCE Model (Better Approaches to Lifestyle and Nutrition for Comprehensive Health) demonstration starting in 2027, which is expected to provide a more structured pathway for GLP-1 obesity coverage within Part D.

This is a time-limited and administratively separate program. Confirm enrollment and eligibility with your Part D plan before July 1, 2026, plans will need to verify your BMI and clinical documentation. The savings card restriction above still applies: even under the Bridge program, Medicare beneficiaries cannot combine the $50 copay with any Lilly manufacturer coupon or discount program.

Medicaid: State-by-State Coverage (2026)

Medicaid coverage for Zepbound is fragmented and narrowing. As of January 2026, only approximately 13 states explicitly cover Zepbound for weight-loss treatment. Several states that previously offered GLP-1 weight-loss coverage have retreated, citing budget constraints:

- California (Medi-Cal): Ended weight-loss GLP-1 coverage effective January 1, 2026. Coverage may still apply for the OSA and type 2 diabetes indications.

- Pennsylvania: Eliminated GLP-1 weight-loss coverage effective January 1, 2026.

- Michigan and New Hampshire: Restricted or ended GLP-1 obesity coverage in the same period.

The practical implication: if you are on Medicaid and were receiving Zepbound for weight management, your coverage may have lapsed at the start of 2026. However, if you have a documented OSA or T2D diagnosis, coverage may still be available under those indications even in states that ended obesity coverage. Check your state’s Preferred Drug List (PDL) directly — search “[Your State] Medicaid preferred drug list” through your state health department. Medicaid patients cannot use the Lilly savings card under any circumstances (see federal exclusion notice above).

How to Get Prior Authorization Approved: 7 Steps

Prior authorization approval rates vary significantly based on how the application is prepared. Over 65% of initial denials are overturned on appeal when full documentation is submitted, which means the documentation quality matters as much as the eligibility criteria themselves.

Step 1: Use a specialist. Prescriptions from endocrinologists or obesity medicine specialists carry meaningfully higher PA approval rates than primary care submissions, approximately three times higher in some analyses. If your primary care physician is submitting the PA, consider requesting a specialist referral or co-signature.

Step 2: Document BMI with a dated clinical measurement. The BMI in the PA must come from a clinical visit note, dated within the last 6 months. A self-reported BMI is not sufficient.

Step 3: Include the correct ICD-10 codes. The combination of codes tells the insurer’s reviewer exactly what medical conditions support the prescription:

- E66.01 — Morbid (severe) obesity due to excess calories

- E11.9 — Type 2 diabetes mellitus without complications

- I10 — Essential (primary) hypertension

- G47.33 — Obstructive sleep apnea (adults)

Step 4: Document ≥6 months of supervised diet and exercise efforts. Include visit notes, registered dietitian records, or documented counseling from at least two provider encounters showing that behavioral interventions were tried and produced insufficient results.

Step 5: Submit a medical necessity letter citing trial data. The letter should reference the SURMOUNT-1 trial results published in the NEJM, specifically the 20.9% mean weight loss at the 15 mg dose at 72 weeks versus 3.1% with placebo, and explain why Zepbound is the medically appropriate choice for this patient.

Step 6: If denied, appeal immediately. Your insurer is required to respond to an appeal within a defined timeframe (typically 30–60 days for standard reviews, 72 hours for urgent cases). More than 65% of denials are reversed on first appeal when proper documentation accompanies the request, according to Pandameds’ analysis.

Step 7: Request a formulary exception for CVS Caremark plans. If Zepbound is not on your plan’s formulary (as is the case for most CVS Caremark plans since July 2025), submit a formulary exception request separate from the standard PA. The exception process allows coverage of a non-formulary drug when the prescriber documents that no formulary alternative is clinically appropriate.

The 2026 Zepbound Savings Card: What Changed

The Eli Lilly Zepbound savings card is the single most impactful cost-reduction tool for commercially insured patients — but the 2026 terms are less favorable than 2025.

| Scenario | 2025 Terms | 2026 Terms |

|---|---|---|

| Commercially insured WITH coverage | As low as $25/mo | As low as $25/mo |

| Annual savings cap | ~$1,950 | ~$1,300 |

| Maximum fills per year | Up to 13 | Up to 13 |

| Commercially insured WITHOUT coverage | As low as $499/mo (single-dose pens) | As low as $499/mo (single-dose pens) |

| Government insured (Medicare, Medicaid, TRICARE, VA) | Not eligible | Not eligible |

Sources: Reddit r/Zepbound savings card update Dec 2025; PrescriberPoint Zepbound savings program

The most significant 2026 change is the reduction in the annual savings cap — from approximately $1,950 in 2025 to approximately $1,300 in 2026. For patients filling 13 times per year at $25/fill, this change limits total annual savings versus last year’s terms. Verify 2026 continuation and current terms directly at Lilly’s savings program page before enrolling, as program terms are subject to change.

For commercially insured patients without Zepbound coverage: A separate savings card reduces the cost to as low as $499/mo for single-dose pens. This is substantially below the $1,086/mo WAC but remains higher than the LillyDirect self-pay options discussed below.

The federal exclusion is absolute. Medicare, Medicaid, TRICARE, and VA beneficiaries cannot use the savings card regardless of indication, dose, or coverage status, see the federal exclusion notice in the Medicare section above.

What If Insurance Doesn’t Cover You? Self-Pay Options

When insurance is unavailable, denied, or simply not worth the administrative fight, there are two credible fallback channels.

LillyDirect Self-Pay (Recommended for Uninsured or Uncovered Patients)

Eli Lilly’s direct-to-consumer platform offers substantially reduced pricing under the Zepbound Self Pay Journey Program. Prices effective December 1, 2025, per CNBC’s reporting on the LillyDirect price cut:

| Dose Strength | LillyDirect Journey Program Price |

|---|---|

| 2.5 mg/mo | $299/mo |

| 5 mg/mo | $399/mo |

| 7.5 mg, 10 mg, 12.5 mg, or 15 mg/mo | $449/mo |

These prices require enrollment in the Self Pay Journey Program and adherence to the program’s refill window. Without enrollment, LillyDirect prices for higher doses are substantially higher (up to $1,049/mo for 15 mg outside the program). Walmart Pharmacy pickup is available for LillyDirect orders at the same pricing as of October 2025.

In February 2026, Lilly launched the Zepbound KwikPen through LillyDirect — a multi-dose, single-patient-use pen containing four weekly doses per pen. KwikPen pricing is comparable to vial pricing ($299–$449/mo under the Journey Program) and is available only through LillyDirect for self-pay patients; it is not yet distributed through traditional pharmacies.

Compare this to the retail list price of $1,086/mo: LillyDirect self-pay saves patients $637–$787/mo depending on dose, without requiring any insurance interaction.

Telehealth Prescription Advantage

A telehealth prescription for Zepbound and a LillyDirect fill are fully compatible. Patients who obtain their Zepbound prescription through a telehealth provider — including through WeightLossInjections.com — can fill that prescription through LillyDirect at self-pay pricing. The prescribing channel is separate from the fill channel.

This matters for patients who want the convenience and clinical support of a telehealth obesity medicine program without giving up access to Lilly’s best pricing. WeightLossInjections.com’s supervised program starts at [$X/month] and includes [service detail], with ongoing prescriber access for dose titration and side effect management, no prior authorization required.

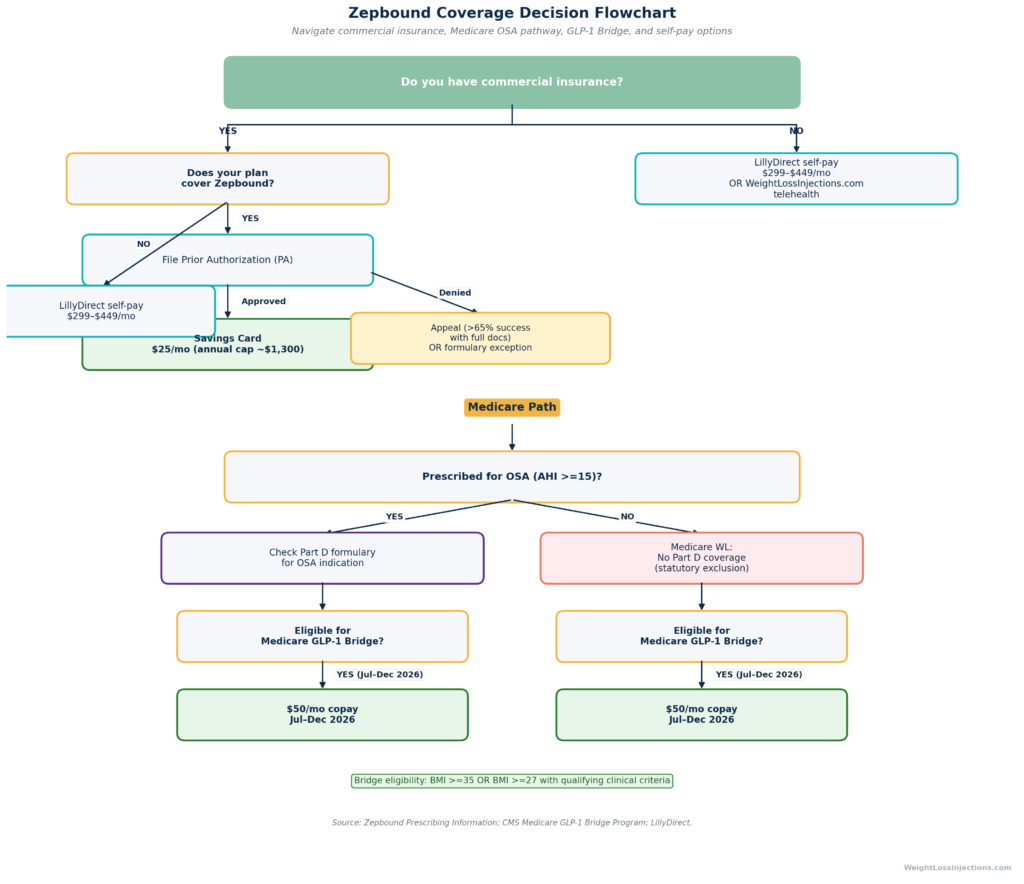

Zepbound Coverage Decision Flowchart

Step-by-Step: Navigating the Prior Authorization Process

Prior authorization does not have to be a black box. Here is what the process looks like from the patient side:

Before your appointment:

Gather your most recent clinical visit notes showing your weight and BMI, any previous weight-management prescriptions (especially if you have tried semaglutide), and records of any comorbidities (hypertension, T2D, dyslipidemia, OSA).

At your appointment:

Ask your prescriber to submit the PA using the ICD-10 codes listed above. Request that they note the SURMOUNT-1 efficacy data in the medical necessity letter, specifically the 20.9% mean weight reduction at 15 mg versus 3.1% placebo from the NEJM 2022 publication, and the FDA-approved indication language from the Zepbound prescribing information.

After submission:

PA timelines vary by payer: typically 3–15 business days for standard review, 1–3 business days for urgent or expedited review. You will receive a determination letter. If denied, the letter must state the specific reason, and that reason is what you respond to in the appeal.

On appeal:

Your prescriber addresses the specific denial reason with targeted documentation. If the denial cites “step therapy not completed,” document the prior medication trial. If the denial cites “BMI not meeting criteria,” provide the clinical measurement. External independent review is available if internal appeals fail, the success rate for external reviews in specialty drug cases is meaningfully positive. Medicaid and Medicare appeals follow different timelines; ask your provider’s office or a patient advocate to help coordinate.

WeightLossInjections.com: Coverage Verification and Telehealth Access

For patients unsure whether their insurance covers Zepbound, WeightLossInjections.com offers a free eligibility check as part of the intake process. Our telehealth providers, board-certified in obesity medicine and endocrinology, review your coverage and, where applicable, assist with prior authorization documentation.

For patients whose insurance does not cover Zepbound or who prefer to avoid the PA process entirely, WeightLossInjections.com’s supervised weight-management program provides access to Zepbound at [$X/month], including [service detail]. Prescriptions can be filled through LillyDirect at self-pay pricing, keeping your monthly cost predictable regardless of insurer decisions.

Our take at WeightLossInjections.com: The 2026 insurance landscape for Zepbound is genuinely better than 2023 and early 2024 — coverage has expanded, the Medicare OSA pathway is now open, and the Bridge program creates a time-limited option for Medicare beneficiaries who would otherwise have no access. But the CVS Caremark formulary removal and the tightening of the savings card cap are real headwinds for commercially insured patients. Our recommendation: if your plan covers Zepbound and you can navigate the PA process, the $25/mo savings card is worth the effort. If your plan denies, your coverage is through a CVS Caremark-managed benefit, or you are on Medicare without OSA, LillyDirect at $299–$449/mo is the most transparent and cost-effective self-pay route available. The telehealth pathway through WeightLossInjections.com gets you a prescription without the PA battle, and LillyDirect pricing still applies.

Frequently Asked Questions

Does insurance cover Zepbound in 2026?

Approximately 43–45% of commercial insurance plans cover Zepbound for weight management (BMI ≥30, or ≥27 with a comorbidity), and about 55% of employer-sponsored plans approve it after prior authorization. Coverage requires BMI documentation and, in most cases, evidence of prior behavioral intervention. CVS Caremark-managed plans removed Zepbound from the standard formulary in July 2025, requiring a formulary exception for coverage. Medicaid covers Zepbound in approximately 13 states for weight loss, though several states, including California, Pennsylvania, Michigan, and New Hampshire, ended or restricted that coverage effective January 1, 2026.

Does Medicare cover Zepbound?

Medicare Part D does not cover Zepbound prescribed solely for weight loss. This prohibition is established by federal statute and applies to all Part D plans — no plan can override it for the obesity/overweight indication. However, since December 2024, Medicare Part D plans may cover Zepbound when prescribed specifically for moderate-to-severe OSA in adults with obesity, subject to individual plan formularies. Additionally, the CMS Medicare GLP-1 Bridge program offers a $50/mo copay for eligible Part D enrollees (BMI ≥35, or ≥27 with clinical criteria) from July 1 through December 31, 2026. This Bridge program operates outside the standard Part D benefit and does not count toward the 2026 Part D out-of-pocket cap of $2,100.

What is the Zepbound savings card for 2026?

The Eli Lilly savings card reduces monthly costs to as little as $25/mo for commercially insured patients whose plans cover Zepbound. The 2026 annual savings cap is approximately $1,300, down from approximately $1,950 in 2025 — with up to 13 fills per calendar year. For commercially insured patients whose plans do not cover Zepbound, a separate savings card reduces costs to as low as $499/mo for single-dose pens. Government-insured patients, Medicare, Medicaid, TRICARE, VA — are not eligible for the savings card under any circumstances. Use of manufacturer coupons by government beneficiaries is prohibited under the federal Anti-Kickback Statute, 42 U.S.C. §1320a-7b.

How do I get Zepbound covered after a denial?

File an appeal with your insurer. Over 65% of initial denials are overturned with complete documentation. The appeal should include: a prescription from an endocrinologist or obesity medicine specialist, a dated clinical BMI measurement, ≥6 months of supervised diet and exercise records, comorbidity ICD-10 codes, and a medical necessity letter citing the SURMOUNT-1 trial data (20.9% weight loss at 15 mg at 72 weeks). If your plan uses CVS Caremark as its PBM, request a formulary exception in addition to or instead of a standard appeal.

What does Zepbound cost without insurance?

Without insurance, the retail list price (WAC) at standard pharmacies is $1,086/mo for all dose strengths. Through LillyDirect’s Self Pay Journey Program, pricing is substantially lower: 2.5 mg ($299/mo), 5 mg ($399/mo), and 7.5–15 mg ($449/mo), per CNBC’s December 2025 reporting on the Lilly price cut. Enrollment in the Journey Program and adherence to the refill window are required.

Can I get Zepbound through a telehealth provider if my insurance doesn’t cover it?

Yes. A telehealth provider can prescribe Zepbound, and you can fill the prescription through LillyDirect at self-pay pricing regardless of the prescribing channel. The prescription origin does not affect LillyDirect eligibility. This makes telehealth an efficient access pathway for patients without coverage: you get clinical oversight and dose management through the telehealth provider, and medication at LillyDirect’s self-pay rates, $299–$449/mo depending on dose, without navigating a PA process. WeightLossInjections.com’s supervised program starts at [$X/month] and includes [service detail].

This article is for informational purposes only and does not constitute medical, legal, or financial advice. Insurance coverage rules, formulary status, savings program terms, and federal policies are subject to change. Verify all pricing, coverage details, and program eligibility directly with your insurer, pharmacy, and Eli Lilly before making treatment decisions. WeightLossInjections.com’s editorial team reviews content quarterly; last verified April 2026.