Comparison chart: “Zepbound Savings Card Tracks 2026”

The Zepbound savings card remains available in 2026 for commercially insured patients, but the terms are materially different from 2025. The annual cap dropped from $1,950 to $1,300, and the monthly maximum savings fell from $150 to $100. Three distinct tracks exist: a covered-benefit track (as low as $25/mo), a non-covered pen track ($499/mo), and a new non-covered KwikPen track ($299–$449/mo). Medicare, Medicaid, VA, and TRICARE beneficiaries cannot use any manufacturer savings card under federal law, separate alternatives exist for each group. Vials have no savings card at all; LillyDirect cash-pay is the only option for that format.

What Is the Zepbound Savings Card?

The Zepbound savings card is a manufacturer copay-assistance program operated by Eli Lilly and Company. It is not insurance, and it does not function like insurance. The card acts as a secondary payer: your commercial insurer processes the claim first, then the savings card covers a portion, up to the monthly cap, of your remaining cost-share.

The program is available to U.S. and Puerto Rico residents who hold active commercial (private) drug insurance. Per the Zepbound savings page at zepbound.lilly.com/savings, the 2026 card is valid through December 31, 2026. Patients who held the 2025 card were auto-updated to 2026 terms; new patients must enroll at zepbound.lilly.com or call 1-866-923-1953. HIPAA authorization is required during enrollment.

The card applies to two delivery formats: the original single-dose auto-injector pen and the multi-dose KwikPen (launched February 23, 2026). It does not apply to Zepbound single-dose vials, vial users must go directly to LillyDirect self-pay pricing at $299–$449/mo depending on dose.

Zepbound must be prescribed for an FDA-approved indication, either chronic weight management in adults with obesity or overweight with a weight-related comorbidity (FDA approval November 8, 2023) or moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity (FDA approval December 20, 2024). Off-label prescriptions are outside the savings card’s scope.

Who Does NOT Qualify for the Savings Card

Before explaining what the card covers, the most critical compliance point deserves its own section.

Manufacturer copay cards, including the Zepbound savings card, cannot be used by beneficiaries of Medicare, Medicaid, TRICARE, the VA, or any other federal or state government healthcare program. This prohibition is rooted in the federal Anti-Kickback Statute (42 U.S.C. § 1320a-7b), which restricts manufacturers from providing financial incentives that could influence decisions around federally funded healthcare. Using a manufacturer card while enrolled in a government program, even as a secondary payer at the pharmacy, can expose patients and pharmacies to compliance risk. This is not a Lilly policy choice; it is a federal statutory requirement documented by the HHS Office of Inspector General.

Programs explicitly barred from using the Zepbound savings card, per zepbound.lilly.com/savings:

- Medicare Part A, Part B, or Part D

- Medicaid (any state or territory)

- TRICARE (all components) / CHAMPUS

- Department of Veterans Affairs (VA) coverage

- Department of Defense (DoD) healthcare programs

- Any state pharmaceutical assistance program funded by government sources

Additional groups who cannot use the savings card:

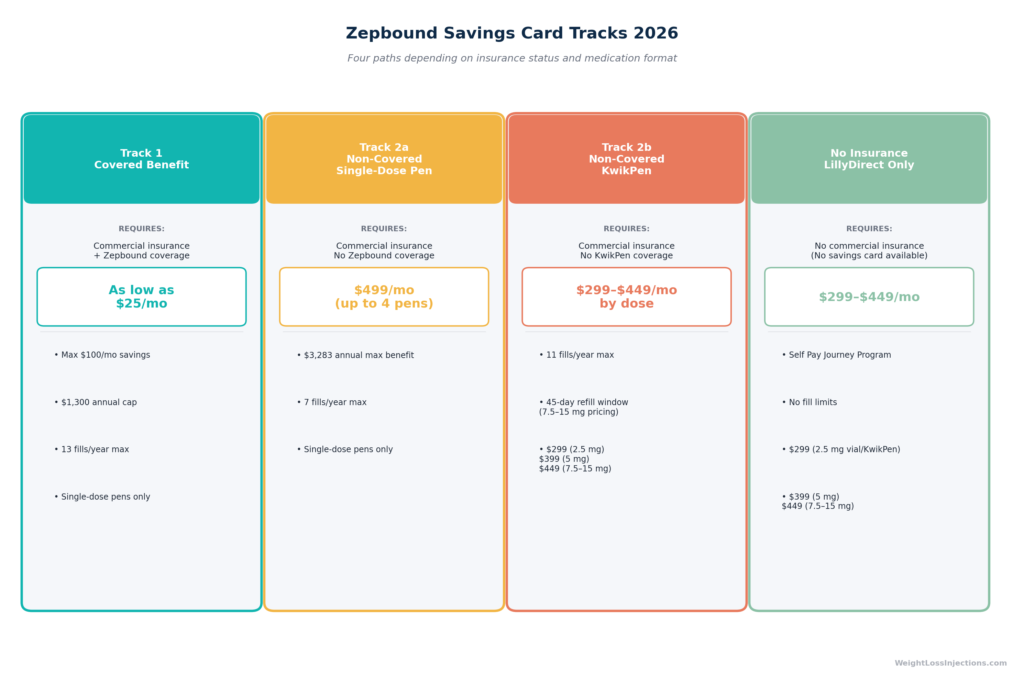

- Uninsured patients. The card requires an active commercial insurance claim to process. Uninsured patients should go directly to LillyDirect at $299–$449/mo — no card required.

- Vial users. Neither savings card track covers the single-dose vial format. Vials are pure self-pay at LillyDirect prices.

- Patients outside the U.S. and Puerto Rico. The program does not extend beyond those jurisdictions.

If you have government insurance, skip to the Medicare Alternatives section — that covers your legitimate savings pathways.

The Three 2026 Savings Card Tracks

The 2026 program has three distinct tracks. Patients fall into exactly one depending on their insurance situation and medication format. Knowing which track applies to you is the difference between $25/mo and $499/mo.

Table: “2025 vs. 2026 Zepbound Savings Card Terms Comparison”

Track 1: Covered Benefit (Commercial Insurance Covers Zepbound)

This is the flagship track, and the one most patients are searching for when they look up the $25/mo price point.

Eligibility: You must have commercial insurance (employer-sponsored, ACA marketplace, or individual commercial plan) that covers Zepbound for an FDA-approved indication. Approximately 43–45% of commercial plans cover Zepbound for weight management, rising to about 55% approval after prior authorization for employer-sponsored plans, per Pandameds insurance coverage analysis from March 2026. Coverage for the OSA indication varies by plan.

Cost structure, per zepbound.lilly.com/savings:

| Fill Length | Patient Pays | Max Card Savings Applied |

|---|---|---|

| 1-month fill | As low as $25 | Up to $100 |

| 2-month fill | As low as $25 | Up to $200 |

| 3-month fill | As low as $25 | Up to $300 |

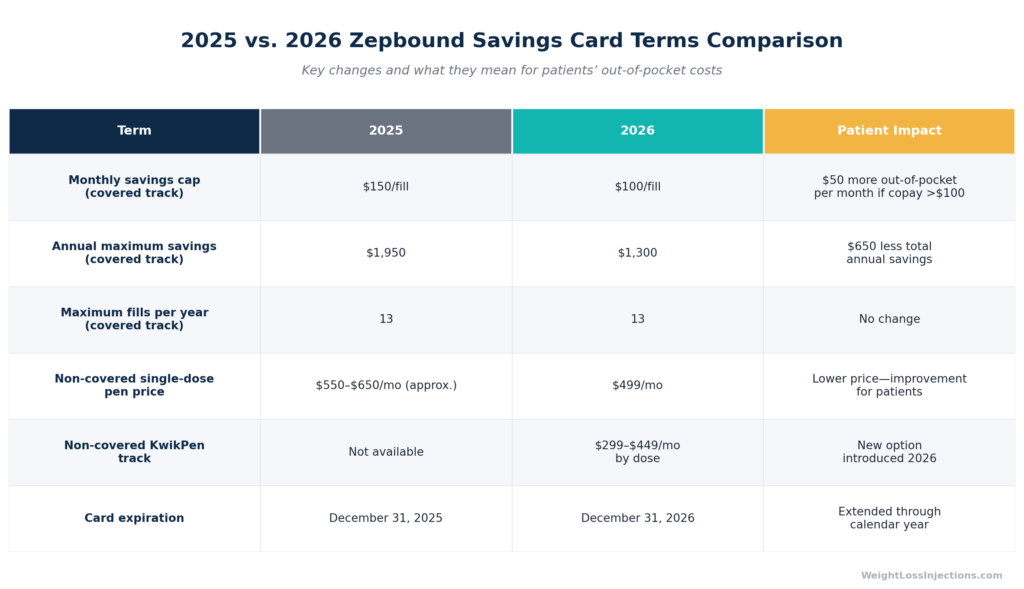

2026 annual cap: $1,300 per calendar year (reduced from $1,950 in 2025). Maximum 13 fills per year. Applies to single-dose pens only.

Practical dollar scenarios: If your insurance copay is $80 before the card, the card covers the entire $80, and you pay $25. If your copay is $125, the card covers $100 and you pay $25. If your copay is $200, the card covers $100 and you pay $100 — not $25. The $25/mo floor only holds when your pre-card copay does not exceed $125. The $100 monthly cap is a hard ceiling on the card’s benefit; the savings card cannot cover your copay dollar-for-dollar beyond that amount.

A note on the cap reduction: The shift from $150/mo to $100/mo in 2026 means patients whose plans have copays in the $100–$150 range will see their out-of-pocket cost rise compared to 2025. A patient with a $150 copay in 2025 paid $25/mo; the same patient in 2026 pays $50/mo. Over a full year (13 fills), the total out-of-pocket increase from the cap change is up to $650, which exactly mirrors the $650 reduction in the annual cap from $1,950 to $1,300.

Savings card payments and your deductible: Most commercial insurance plans do not count manufacturer savings card payments toward your deductible or out-of-pocket maximum. This is a common misconception. Confirm with your specific insurer, but in the majority of plans, the card reduces your copay without helping you reach your deductible.

Track 2a: Non-Covered Benefit, Single-Dose Pens

Eligibility: Commercially insured patients whose plan does not cover Zepbound for any indication.

Cost: $499/mo for up to four single-dose pens (one month’s supply, all dose strengths from 2.5 mg through 15 mg), per PrescriberPoint Zepbound non-covered benefit data and zepbound.lilly.com/savings.

Annual parameters: Maximum annual benefit of $3,283; up to 7 fills per calendar year.

Important comparison: At $499/mo for the non-covered pen track, LillyDirect’s KwikPen pricing of $299–$449/mo (depending on dose) may be cheaper for patients at 7.5 mg or higher, and the KwikPen non-covered savings card (Track 2b below) offers the same pricing without requiring you to bypass your insurance. Patients on this track should compare before assuming the pen track is their only option.

Track 2b: Non-Covered Benefit, KwikPen (New for 2026)

The multi-dose KwikPen launched on February 23, 2026, and Lilly introduced a corresponding non-covered savings card track at the same time, per CNBC’s reporting on the KwikPen launch.

Eligibility: Commercially insured patients whose plan does not cover the Zepbound KwikPen.

Cost by dose, per zepbound.lilly.com/savings:

| Dose Strength | Monthly Cost (Non-Covered KwikPen Track) |

|---|---|

| 2.5 mg | $299/mo |

| 5 mg | $399/mo |

| 7.5 mg | $449/mo |

| 10 mg | $449/mo |

| 12.5 mg | $449/mo |

| 15 mg | $449/mo |

Annual parameters: Maximum 11 fills per calendar year.

45-day refill requirement: For patients using the 7.5–15 mg KwikPen at $449/mo pricing under the Purchase Offer Terms, the 45-day refill window must be observed for pricing continuity. Filling before the 45-day mark can disrupt program eligibility; confirm timing with your pharmacy.

KwikPen format note: The KwikPen contains four weekly doses in a single multi-dose, single-patient-use pen, eliminating the need to handle four separate pens per month. It requires priming before each use and is currently available only through LillyDirect for self-pay patients and through the non-covered savings card track.

2026 vs. 2025: What Changed and Why It Matters

The 2026 card represents a meaningful reduction in the covered-benefit track’s value compared to 2025. The table in Image 2 above summarizes the changes; here is the practical interpretation.

The monthly cap reduction from $150 to $100 is the most impactful change for patients with mid-range copays. A patient whose insurer sets a $140/mo copay for Zepbound saved the full $140 under the 2025 card (leaving them at $25 to pay). Under the 2026 terms, the card covers only $100 of that $140 copay, leaving the patient with $40/mo out-of-pocket rather than $25. Across a full year, that’s a $195 increase in costs even before accounting for the lower annual cap.

For patients with very high copays (above $150), the practical impact is smaller in absolute terms because both the 2025 and 2026 cards hit their respective ceilings without closing the gap to $25.

The non-covered pen track improved in 2026, with the price dropping to a flat $499/mo from an estimated $550–$650 range in 2025. And the addition of the KwikPen non-covered track at $299–$449/mo is a genuine new option that did not exist last year.

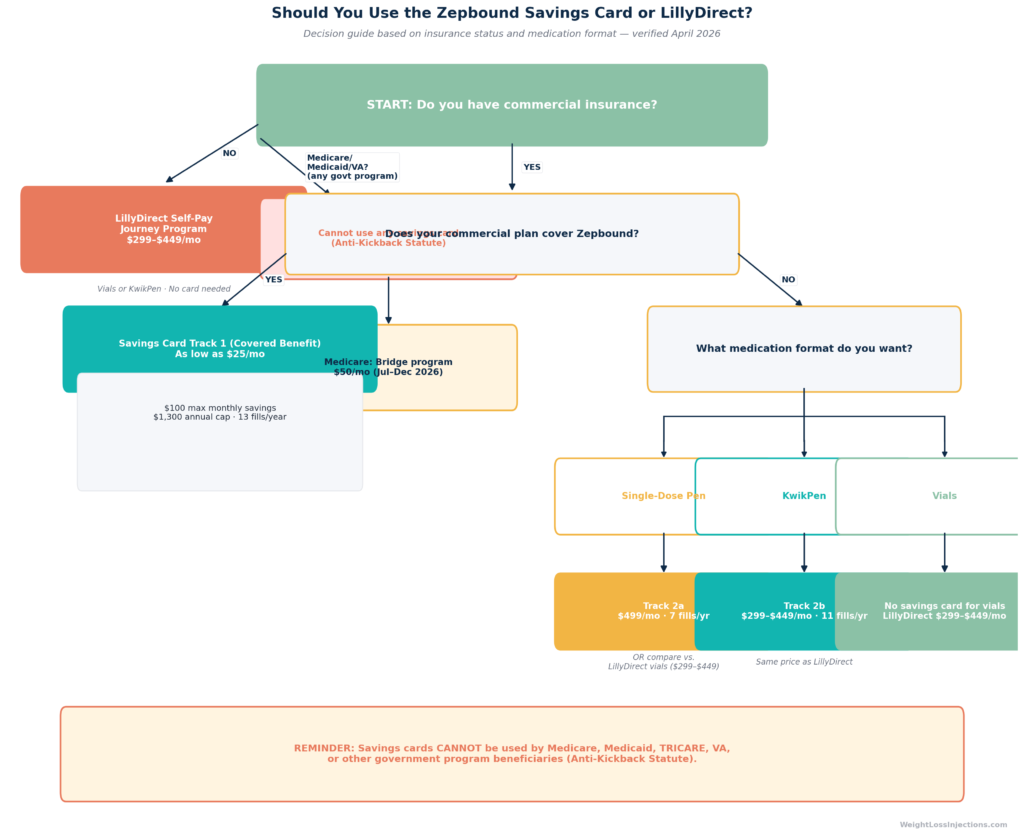

Savings Card vs. LillyDirect: Which Pathway Is Right for You?

Not every patient should default to the savings card. The right pathway depends on your insurance status, the dose you’re prescribed, and your preferred medication format.

Flowchart: “Should You Use the Savings Card or LillyDirect?”

When the Covered Track (Track 1) Is Clearly the Right Choice

If your commercial plan covers Zepbound and your copay is $125 or less, the covered-benefit savings card brings your out-of-pocket down to $25/mo. This is the optimal outcome and the case where the card provides the most value. Use the card.

If your copay is higher, say $200 or $300, the card still saves you $100/mo (on a 1-month fill), which is meaningful. Whether you accept that or push for a prior authorization appeal to get your copay reduced is a separate clinical conversation with your prescriber.

When to Bypass the Savings Card and Use LillyDirect

Non-covered patients at higher doses: If your plan doesn’t cover Zepbound and you’re prescribed 7.5 mg or higher, Track 2a costs $499/mo for pens. LillyDirect’s Self Pay Journey Program offers vials at $449/mo for the same doses, $50/mo less than Track 2a, with no fill-count limit. The KwikPen through Track 2b also prices at $449/mo for 7.5–15 mg doses, matching LillyDirect pricing, but caps you at 11 fills per year vs. no cap on LillyDirect.

Uninsured patients: No savings card exists for this group. Go directly to LillyDirect for vials or the KwikPen at $299–$449/mo depending on dose. You can also pick up LillyDirect-priced vials at Walmart Pharmacy locations nationwide.

Patients who prefer the vial format: There is no savings card for vials under any track. LillyDirect is the only pricing mechanism, $299/mo (2.5 mg), $399/mo (5 mg), or $449/mo (7.5–15 mg) with Self Pay Journey Program enrollment, per CNBC’s December 1, 2025 reporting on the LillyDirect price cut. Vials require a separate syringe and needle (purchased separately) and are not available for pickup at retail pharmacies outside the LillyDirect/Walmart arrangement.

LillyDirect Self-Pay Journey Program: The Key Enrollment Requirement

The $449/mo flat pricing for 7.5–15 mg doses on LillyDirect requires enrollment in the Self Pay Journey Program and adherence to the refill window. Without program enrollment, LillyDirect’s regular self-pay prices for higher doses are substantially higher, $599 for 7.5 mg, $699 for 10 mg, $849 for 12.5 mg, and $1,049 for 15 mg. The program enrollment step is not optional if you want the $449/mo price; confirm enrollment status before your first fill at those dose strengths.

Medicare Alternatives for 2026

Medicare beneficiaries are categorically excluded from the manufacturer savings card under the Anti-Kickback Statute (42 U.S.C. § 1320a-7b). This is not a gap in the law or a technicality, it is explicit, and there are no exceptions. But two separate options exist for 2026.

Medicare GLP-1 Bridge Program (July 1 – December 31, 2026)

CMS announced a short-term Medicare GLP-1 Bridge program under which Medicare Part D beneficiaries can access Zepbound for obesity at a $50/month copayment. Per KFF analysis from March 2026:

- Eligibility: BMI ≥35, or BMI ≥27 with qualifying clinical criteria

- Duration: July 1 through December 31, 2026 only — this is a time-limited bridge program

- How it operates: Outside the standard Part D benefit — payments do not count toward the $2,100 Part D out-of-pocket cap for 2026

- Purpose: Bridges beneficiaries to the BALANCE Model demonstration starting in 2027

If you have Medicare Part D and meet the BMI criteria, the Bridge program at $50/mo is significantly more affordable than any private-market alternative. Contact your Part D plan to confirm enrollment procedures; the program structure requires plan participation.

Medicare Part D — OSA Indication

If Zepbound is prescribed specifically for moderate-to-severe obstructive sleep apnea (the second FDA-approved indication, approved December 20, 2024), Medicare Part D plans may cover it at standard formulary cost-sharing rates. Per Wellcare Medicare guidance, formulary coverage varies by plan. This is worth pursuing if you have an OSA diagnosis that meets the clinical criteria for Zepbound, since the standard Part D benefit has a $2,100 OOP cap in 2026 under the Inflation Reduction Act.

Note: Medicare is statutorily prohibited from covering Zepbound under Part D for the obesity/weight management indication alone. Per American College of Gastroenterology reporting from April 2025, anti-obesity drugs will not be covered by Medicare and Medicaid under the weight loss indication in 2026. The OSA coverage pathway is a separate clinical track.

How to Enroll in the Zepbound Savings Card: Step-by-Step

Step 1: Confirm Eligibility

Before enrolling, verify two things. First, confirm you have commercial insurance, not Medicare, Medicaid, VA, TRICARE, or any government-funded plan. Second, confirm Zepbound is prescribed for an FDA-approved indication (weight management or OSA). If you are unsure whether your plan is commercial or government-funded, call the member services number on your insurance card and ask directly.

Step 2: Activate Your Card

Enroll online at zepbound.lilly.com/savings or call 1-866-923-1953. Have your insurance information and date of birth ready. HIPAA authorization is required during the enrollment process. Existing cardholders from 2025 were auto-updated to 2026 terms; no re-enrollment is required unless your insurance situation changed.

Step 3: Determine Your Track at the Pharmacy

When you present at the pharmacy, tell the pharmacist: “Please run my insurance first, then apply the Zepbound manufacturer savings card as a secondary.” This is the standard process, insurance processes the primary claim, the savings card then applies to your remaining copay or coinsurance. Not all pharmacy staff are equally familiar with this two-step process; having the phrase ready prevents errors.

For the non-covered tracks (2a or 2b), your insurance will process the claim, reflect no coverage for Zepbound, and the non-covered savings card price will apply to your out-of-pocket cost at participating pharmacies.

Step 4: Track Your Annual Cap

The covered-benefit track has a $1,300 annual cap and a maximum of 13 fills per calendar year. Track your remaining annual savings — if you exhaust the $1,300 cap before December 31, you will pay your full copay for remaining 2026 fills. The card resets January 1 each year. If your insurance situation changes mid-year (e.g., you switch employers), contact 1-866-923-1953 to update your enrollment.

What the Savings Card Does Not Cover: Common Patient Misconceptions

Misconception 1: “The savings card brings my cost to $25 no matter what my copay is.”

False. The card covers up to $100 per 1-month fill. If your copay is $300, you pay $200 — not $25. The $25 floor only applies when your pre-card copay is $125 or less.

Misconception 2: “The savings card works with my Medicare Advantage plan.”

False. Medicare Advantage plans are Medicare programs. They are prohibited from using manufacturer savings cards under the Anti-Kickback Statute (42 U.S.C. § 1320a-7b), regardless of whether the plan is administered by a private insurer.

Misconception 3: “The savings card payments count toward my deductible.”

In most commercial insurance plans, manufacturer copay assistance card payments do not count toward your deductible or annual out-of-pocket maximum. Some plans have adopted “copay accumulator” or “copay maximizer” programs that specifically exclude third-party payments from accumulating toward deductibles. Check your plan’s Summary of Benefits and Coverage (SBC) or call your insurer to confirm how the Zepbound savings card payments are treated.

Misconception 4: “I can use the savings card for vials from LillyDirect.”

False. Neither the covered-benefit track nor either non-covered track applies to Zepbound single-dose vials. Vials are only available through LillyDirect as a cash-pay product with no savings card mechanism.

Misconception 5: “The savings card and a pharmacy discount card like GoodRx can be combined.”

False. GoodRx and similar discount cards represent an alternative cash-pay pricing track that bypasses insurance entirely. The Zepbound savings card requires an insurance claim to apply. They operate on incompatible billing tracks and cannot be stacked.

Our Take at WeightLossInjections.com

Our take at WeightLossInjections.com: The 2026 savings card changes are real and consequential for a meaningful subset of patients, particularly those whose copays fall in the $100–$150 range, who will see their monthly cost increase noticeably compared to 2025. The coverage landscape is also fragmented in a way that makes it genuinely difficult for patients to self-navigate: three savings card tracks, a LillyDirect pathway with its own enrollment requirements, a Medicare Bridge program that runs only for six months, and a hard prohibition on manufacturer card use for government-program beneficiaries that isn’t always communicated clearly at the pharmacy counter.

The most common expensive mistake we see is patients on Medicare asking their pharmacy to apply a manufacturer savings card, the pharmacy may decline it, apply it incorrectly, or create a compliance issue, and the patient leaves confused about why their “discount” didn’t work. If you are on Medicare, the Bridge program at $50/mo (July–December 2026) is your savings pathway, not the Lilly card.

WeightLossInjections.com provides licensed prescriber access to FDA-approved Zepbound starting at [$X/month], including [service detail]. Every patient intake includes an insurance status screening to identify the correct savings pathway before your first fill, so you’re not discovering mid-pharmacy-visit that you’re on the wrong track. We do not offer compounded tirzepatide; both the 503A and 503B compounding windows are closed as of April 2026. Only branded, FDA-approved Zepbound from licensed pharmacies. [Start your intake →]

Frequently Asked Questions

How do I get the Zepbound savings card for 2026?

Enroll online at zepbound.lilly.com/savings or call 1-866-923-1953. HIPAA authorization is required during enrollment. If you held a 2025 savings card, you were automatically updated to 2026 terms, re-enrollment is not required unless your insurance changed. New patients need to enroll before presenting at the pharmacy; the card cannot be applied retroactively to a fill that already processed.

Who qualifies for the $25/month Zepbound savings card?

The $25/mo cost is available through Track 1 (covered benefit) to patients who: (1) have active commercial insurance that covers Zepbound for an FDA-approved indication; (2) reside in the U.S. or Puerto Rico; and (3) are not enrolled in Medicare, Medicaid, VA, TRICARE, DoD, or any government-funded healthcare program. The $25/mo floor only applies when your insurance copay before the card is $125 or less, if your copay exceeds $125, the card covers $100 of it and you pay the remainder. The 2026 annual maximum savings is $1,300, so after 13 fills or $1,300 in card benefit (whichever comes first), you pay your full copay for the rest of the calendar year.

Does the Zepbound savings card work with Medicare?

No. Manufacturer savings cards, including the Zepbound savings card, cannot be used by Medicare beneficiaries. This prohibition is mandated by the federal Anti-Kickback Statute (42 U.S.C. § 1320a-7b). It applies to all Medicare coverage types, including Medicare Advantage plans administered by private insurers. If you have Medicare, your savings pathways are: (1) the Medicare GLP-1 Bridge program at $50/mo copayment for eligible beneficiaries (July 1–December 31, 2026, per KFF analysis); or (2) Part D coverage for the OSA indication if your plan formulary covers it.

Can I use the savings card for Zepbound vials?

No. Neither the covered-benefit track nor either non-covered track applies to Zepbound single-dose vials. Vials are exclusively a LillyDirect self-pay product, priced at $299/mo (2.5 mg), $399/mo (5 mg), or $449/mo (7.5–15 mg) through the Self Pay Journey Program, per CNBC’s reporting on the December 1, 2025 price reduction. Vials also require a separate syringe and needle and cannot be picked up at traditional retail pharmacies outside the LillyDirect/Walmart arrangement.

What happens if my copay is higher than the $100 monthly savings cap?

The card covers exactly $100 (for a 1-month fill) of your remaining copay after insurance processes. If your copay is $200, the card pays $100 and you pay $100. If your copay is $400, the card pays $100 and you pay $300. There is no mechanism to exceed the $100 monthly cap on the covered-benefit track. In this scenario, patients have two options: (1) work with their prescriber to appeal for a lower copay tier through prior authorization or plan exception; or (2) compare whether the non-covered LillyDirect self-pay price at $449/mo for higher doses makes financial sense relative to the partially reduced insured price.

Do existing savings card holders need to re-enroll for 2026?

Existing cardholders were automatically updated to 2026 program terms by Eli Lilly, no action required for most patients. However, if your insurance changed since last enrollment (new employer, new plan, change in coverage for Zepbound), contact 1-866-923-1953 or return to zepbound.lilly.com/savings to update your enrollment. The 2026 annual cap reset on January 1, 2026; your savings counter started fresh regardless of when you last used the card in 2025.

This article is for informational purposes only and does not constitute medical or legal advice. Savings card terms, eligibility rules, and pricing are subject to change by Eli Lilly at any time without notice. All figures are verified against primary sources as of April 2026. WeightLossInjections.com reviews content quarterly; last verified April 2026. Always confirm current program terms directly with Eli Lilly (1-866-923-1953) or at zepbound.lilly.com/savings before making coverage or access decisions.